In leasing commercial real estate, office or company-housing from a foreign owner (a non-resident owner), the Japanese tax agency requires lessees to pay withholding tax on behalf of the owners abroad. It means the lessee needs to pay the withheld tax every month (by the 10th of the following month) as well as paying monthly rent. This extra work of having to do tax-withholding tends to be a concern when people (under the company lease) search for rental properties, and it may cause a disadvantage for a non-resident. In this situation, master leases provide a solution so that lessees can exempt the tax-withholding procedure.

What is a Master Lease / Sublease?

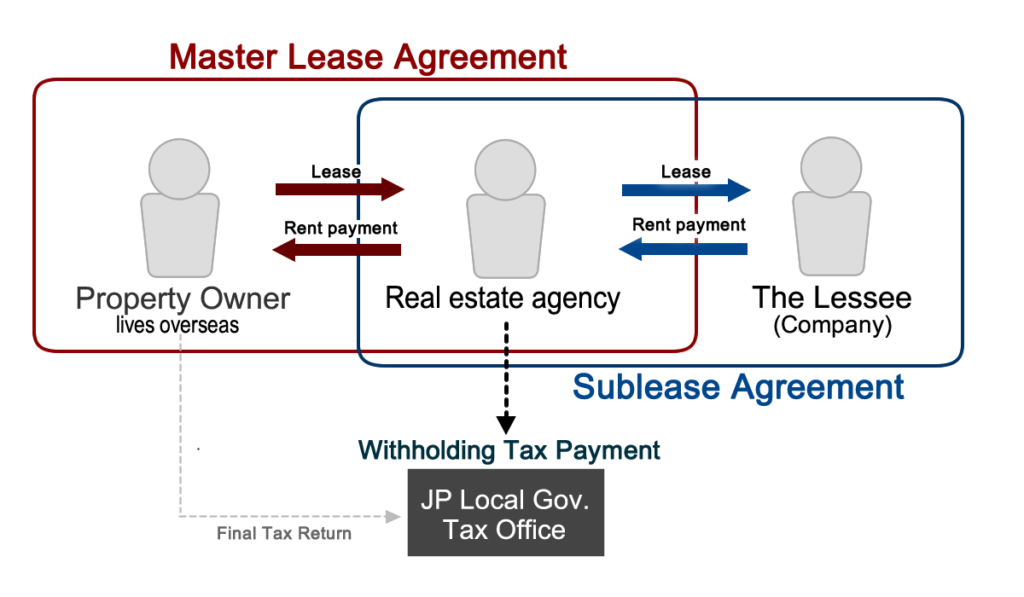

Master lease/sublease is a type of lease structure arranged for rental agreement in real estate. In this arrangement here described, a real estate agency (subleasing company) comes in between the property owner and the tenant, and the three parties sign a lease contract with each other. A master lease is where the real estate agency leases a rental property (e.g. office building) from the property owner. A sublease is where the real estate company subleases the property to the Lessee who use the rental property, shown below as a company being “The lessee.”

How does a master lease/sublease work?

Under a master lease agreement, the real estate agency is responsible for the property’s management. The agency takes on the management role, and the property owner has almost no responsibility for daily operations. If trouble happens with a tenant, the property owner may avoid direct involvement from such a problem. On the other hand, the owner is not be able to sign a contract directly with a tenant, and two arrangements are to be made through the real estate agency.

Advantage of master lease/sublease in leasing a non-resident owner property

When it comes to leasing a residential/commercial property from a foreign owner (non-resident owner), a master lease/sublease brings an advantage that the lessees will be exempt from withholding tax and the payment, which are usually required.

From a lessee’s perspective

Having to withhold tax from monthly rent is extra work for the Lessee, that they would like to avoid as much as possible. In subleasing from a real estate agency, the lessee will not be required to pay for the withholding tax. Under a master lease agreement between the non-resident owners, and a real estate agency, the agency will become the Lessor of the property. Therefore, the real estate agency requires to withhold and pay the tax as a master tenant on behalf of the property owner. What the Lessee needs to do is to pay the monthly rent based on the lease agreement.

Non-resident owners, often own high-end properties. You may find another advantage: people with a company lease can search for rental properties from a better, wider choice if they don’t need to consider tax-withholding.

From a property owner’s perspective

Relieving from the disadvantage of tax-withholding may encourage companies to lease a property from Non-resident owners, where the owner can expect a higher close rate. Large corporate/companies, who intend to minimize back-office work, such as tax payment, intend to avoid signing a lease contract with the property requires tax-withholding payment. However, a sublease allows those corporate/companies able to sign a lease agreement. Under the sublease structure, Non-resident owners in possession of high rental properties will have more chance to find a prospective tenant.

What’s tax withholding required?

Withholding tax on rental income means that a tenant who leases real estate from a non-resident is required to withhold tax on the rental fee and pay it to the local tax office in Japan on behalf of the owner. Tax-withholding is required only for a company lease (residential, commercial properties). It is not applied to rental properties which individual lease for personal use. The taxation is 20.42% that includes “Income tax and Special income tax for reconstruction.” (所得税及び復興特別所得税)

To find more detailed information, please refer to this article:

Rental properties in Japan | Paying tax on rent on behalf of a foreign owner

https://living.rise-corp.tokyo/withholding-tax-on-rent/

Master lease payment options

Under a master lease agreement, the property owner has two options to receive rents from the real estate agency; “Fixed-rent” and “linked-rent.”

Under the contract on a “Fixed-rent basis” (Akishitu-hoso空室保証型), the property owner is guaranteed to receive a certain amount of fixed rent payment. The real estate agency, which leases a rental property (residential or commercial etc.), is to pay the owner the rent regardless of the vacancy. On the other hand, the property can retain only a fixed income, which means it will not be able to maximize the profitability.

The “Linked rent basis” (Jisseki-rendo gata 実績連動型) is more likely recognized as Percentage-rent. In this payment system, the owner may receive rent in accordance with the number of tenants. For example, if the rental building has ten office rooms and the real estate agency operates it and has five tenants, the owner receives rent from the agency calculated as; 5 x Rental-fee. If having ten tenants, the owner receives rent: 10 x Rental-fee. The owner can obtain higher rental income when there is less vacancy.

Real estate agencies that manage master lease/sublease transactions are recently declining in number as it involves much of the management process and the involvements. However, it is still an option that can support both the non-resident owners and the lessee to meet compliance without the tax-withholding procedure.

Rent & Sales Property

RISE Corp Channel